Among the predictable Republican reactions to the President's proposed 2013 budget is the refrain that "Obama has failed to keep a 2009 promise to cut the deficit in half by the end of his first term." Just days after Senate Minority Leader Mitch McConnell told a CPAC audience that President Obama "said he'd cut the deficit in half by the end of his first term," ABC's Jake Tapper dutifully announced "Obama's broken deficit promise." And today, the RNC debuted a new ad in which a supposedly betrayed voter warns, "President Obama, you broke your promise. I'll never forget that."

Of course, what everyone seems to be forgetting is that in 2004 President George W. Bush promised - and failed - to halve the federal budget deficit by 2009. As it turns out, Bush broke his pledge even before the economic cataclysm of 2008 that triggered the TARP bank bailout, sent government revenues plummeting, and required President Obama's rescue programs that saved the U.S. from "Greet Depression 2.0."

As he faced reelection in 2004, George W. Bush famously committed to cut the deficit in half by 2009. As it turned out, the budget Bush bequeathed to Barack Obama didn't even get close to that target. The FY 2009 budget Bush proposed in February 2008 called for a deficit of roughly $400 billion, almost identical to the result in 2004. But that January 2004 promise, as the Washington Post, CNN and The New York Times among others noted at the time, was premised upon two parallel frauds. As Perrspectives explained four years ago:

First, Bush's pompous prediction used as its baseline a wildly inflated White House deficit forecast of $521 billion, well above the CBO's estimate and the actual figure of $413 billion. More importantly, President Bush conveniently chose 2009 as his finish line, the year before his tax cuts were set to expire. Making them permanent (which he and all of the GOP presidential candidates endorse) would blow another $2.2 trillion hole in the federal budget by 2014.

(It's also worth noting, as the Obama administration has this week, that Bush's budget plans always understated the real deficit, because they routinely failed "to account for the costs of the wars in Afghanistan, the cost of preventing cuts to Medicare doctors, and the price of staving off an expansion of the alternative minimum tax.")

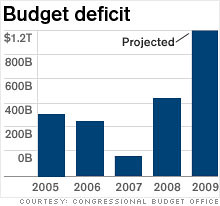

But the Bush recession that began in December 2007 made all of his budget targets — and those followed — moot. With federal tax revenues already declining, in the fall of 2008 Congress passed and President Bush signed the $700 billion Troubled Asset Relief Program (TARP). The first $350 billion was distributed to the largest U.S. banks on October 3, 2008, two days after the start of fiscal year 2009. The result is that when President Obama took the oath of office on January 20, 2009, the Congressional Budget Office (CBO) revised its FY 2009 deficit to $1.2 trillion. As CNN reported on January 7, 2009:

The U.S. budget deficit in 2009 is projected to spike to a record $1.2 trillion, or 8.3% of gross domestic product, the Congressional Budget Office said Wednesday.

The dramatic jump to the highest-ever deficit in dollar terms compares to a $455 billion deficit in fiscal year 2008.

As President Obama's 2013 budget submission released this week explained:

The result was that, upon taking office, the President faced an annual deficit of $1.3 trillion, or 9.2 percent of GDP, and a 10-year deficit of more than $8 trillion -- and this figure grew even larger as the depth of the recession became clear.

As it turned out, the economy President Obama inherited was in much worse shape than realized at the time. President Obama's $787 billion stimulus package and pledge to halve the trillion dollar plus deficit by the end of his first term came in February 2009, long before the full magnitude of the U.S. economic collapse was clearly known. As The Economist explained last year:

The White House looked at the economic situation, sized up Congress, and took its shot. Unfortunately, the situation was far more dire than anyone in the administration or in Congress supposed.

Output in the third and fourth quarters fell by 3.7% and 8.9%, respectively, not at 0.5% and 3.8% as believed at the time. Employment was also falling much faster than estimated. Some 820,000 jobs were lost in January, rather than the 598,000 then reported. In the three months prior to the passage of stimulus, the economy cut loose 2.2m workers, not 1.8m. In January, total employment was already 1m workers below the level shown in the official data.

The four consecutive trillion dollar deficits don't merely reflect the past and proposed economic stimulus measures the Obama White House has advocated. Federal tax revenue ($2.9 trillion), which as a percentage of the U.S. economy hit its lowest level in 60 years in 2010, is only now surpassing to its pre-recession peak ($2.6 trillion in 2007). (The extension of the Bush tax cuts for the wealthy is not helping matters.)

All of which explains the numbers that Jake Tapper of ABC presented largely context-free in recalling Barack Obama's February 2009 pledge to "cut the deficit we inherited in half by the end of my first term in office."

The 2013 budget the president submitted today does not come close to meeting this promise of being reduced to $650 billion for fiscal year 2013.

The president noted in that 2009 speech the Obama administration inherited a $1.3 trillion deficit.

The deficit was similarly $1.3 trillion in 2011, is projected to be $1.15 trillion in 2012, and the president's budget claims it will be $901 billion in 2013.

Tapper is right, of course, that President Obama will miss his target. The devastation of the Bush recession which commenced in late 2007 was worse and the U.S. economic recovery much slower than Team Obama forecast three years ago. In a nutshell, that's why Barack Obama will — and should — follow in George W. Bush's footsteps in failing to keep an optimistic promise about cutting the annual federal deficit by half.

(This piece also appears at Perrspectives.)