It was the best of times, it was the worst of times. Just for different groups of Americans. That's the picture emerging from a wave of stories about the depths of the American economic downturn. On the same day The Economist revealed that the U.S. economic contraction beginning in late 2007 was far deeper than originally thought, new IRS data showed that Americans' average income plummeted by almost 14% in 2009 compared to two years earlier. For most, employment and incomes have yet to recover. But for the gilded class, things are apparently back to normal.

As The Economist explained, the Bush recession Barack Obama inherited in January 2009 was far more severe than previously understood:

The White House looked at the economic situation, sized up Congress, and took its shot. Unfortunately, the situation was far more dire than anyone in the administration or in Congress supposed.

Output in the third and fourth quarters fell by 3.7% and 8.9%, respectively, not at 0.5% and 3.8% as believed at the time. Employment was also falling much faster than estimated. Some 820,000 jobs were lost in January, rather than the 598,000 then reported. In the three months prior to the passage of stimulus, the economy cut loose 2.2m workers, not 1.8m. In January, total employment was already 1m workers below the level shown in the official data.

Whether that information might have led to a much larger stimulus package in February 2009 is impossible to know. But what's clear is the toll the deepening Bush recession took on American households that year. As Reuters explained:

Average income in 2009 fell to $54,283, down $3,516, or 6.1 percent in real terms compared with 2008, the first Internal Revenue Service analysis of 2009 tax returns showed. Compared with 2007, average income was down $8,588 or 13.7 percent.

Average income in 2009 was at its lowest level since 1997 when it was $54,265 in 2009 dollars, just $18 less than in 2009.

That dip is explained in part by the temporary loss in stock market and other asset wealth for the three percent of Americans who earned over $200,000 a year. And it probably has a lot to do with the fact that in 2009, as Politico reported, a rising number of millionaires paid no taxes at all:

Though the tax rate for Americans earning a gross adjusted income of $1 million or more averaged 24.4 percent, up from 23.1 percent in 2008, that's still lower than the 28.5 percent rate they paid in 2002 when President George W. Bush was in office.

And, the data shows, the 235,413 taxpayers who reported earning seven digits or more in 2009 took in a total of $726.9 billion -- yet 1,470 paid not a penny of income taxes. In 2007, 959 Americans earning $1 million or more paid no income taxes.

But while America's so-called "job creators" didn't create jobs after receiving their decade-long Bush tax cut windfall, they did buy a lot of expensive shoes. That's word from the New York Times, which reported Wednesday that "sales of luxury goods are recovering strongly":

Nordstrom has a waiting list for a Chanel sequined tweed coat with a $9,010 price. Neiman Marcus has sold out in almost every size of Christian Louboutin "Bianca" platform pumps, at $775 a pair. Mercedes-Benz said it sold more cars last month in the United States than it had in any July in five years.

Even with the economy in a funk and many Americans pulling back on spending, the rich are again buying designer clothing, luxury cars and about anything that catches their fancy. Luxury goods stores, which fared much worse than other retailers in the recession, are more than recovering -- they are zooming. Many high-end businesses are even able to mark up, rather than discount, items to attract customers who equate quality with price.

As Arnold Aronson, managing director of retail strategies at the consulting firm Kurt Salmon, put it, "If a designer shoe goes up from $800 to $860, who notices?"

Certainly not America's rich and famous. After all, the recession that has proved so devastating for most Americans for the wealthy has been merely a hiccup.

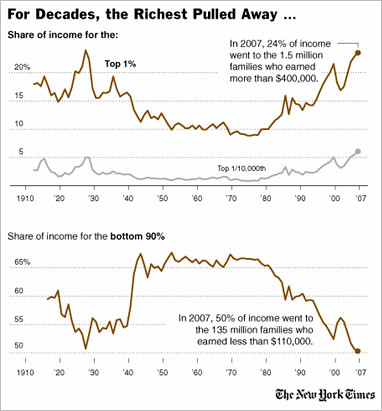

Two years ago, David Leonhardt and Geraldine Fabrikant of the New York Times concluded, "After a 30-year run, [the] rise of the super-rich hits a sobering wall."

They began to pull away from everyone else in the 1970s. By 2006, income was more concentrated at the top than it had been since the late 1920s. The recent news about resurgent Wall Street pay has seemed to suggest that not even the Great Recession could reverse the rise in income inequality.

But economists say -- and data is beginning to show -- that a significant change may in fact be under way. The rich, as a group, are no longer getting richer. Over the last two years, they have become poorer. And many may not return to their old levels of wealth and income anytime soon.

As it turned out, that time wasn't just soon. It's now.

The Los Angeles Timesa> announced the return of record-setting income inequality in June 2010 in an article titled, "Millionaires Make a Comeback." After getting pummeled as Wall Street plummeted in 2008, the rich have begun to recoup their losses. The short period of Gilded Interrupted is over:

In 2008, as the financial crisis raged, the stock market hit bottom and the Great Recession ate into the economy, the number of millionaires in the United States plunged.

But last year the number of millionaires bounced up sharply, new data show.

And after that decline and rebound, the millionaire class held a larger percentage of the country's wealth than it did in 2007.

"It's been a recession where everyone took a hit -- with the bottom taking a bigger hit," said Timothy Smeeding, a University of Wisconsin professor who studies economic inequality. But "the wealthy alone have bounced back."

Bounced back, it turns out, with a vengeance. The Boston Consulting Group found that "the number of U.S. households with at least $1 million in "bankable" assets climbed 15 percent last year to 4.7 million after tumbling 21 percent in 2008." Despite there being 10 percent fewer millionaires than in 2007, the percentage of Americans' total wealth held by those households was slightly higher, growing to 55 percent. Executive pay rose by 23 percent last year. By last summer, the Wall Street Journal proudly proclaimed, "U.S. Economy Is Increasingly Tied to the Rich." As a recent Deloitte presentation for wealth managers forecast:

Our analysis indicates that aggregate wealth of millionaire households in the U.S. in 2020 will likely reach $87 trillion, from $39 trillion in 2011.

GOP White House hopeful Michele Bachmann need not have worried, as she did in 2009, that:

"We're running out of rich people in this country."

Writing in the Washington Post last summer, Ezra Klein neatly summed up the dynamic which has restored income inequality to record highs even as the U.S. economy struggles to recover:

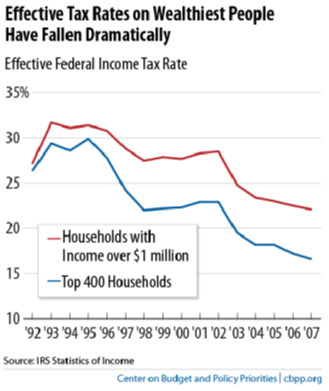

The basic story here is that assets have recovered so much more quickly than the broader economy that in 2009, "the millionaire class held a larger percentage of the country's wealth than it did in 2007." In other words, inequality has actually gotten worse. If you want to see why that's unexpected, check out the chart I cadged from the Center for Budget and Policy Priorities: After the Great Depression, inequality fell and didn't recover until 2007. That's about 80 years. After the Great Recession, inequality fell and didn't recover until ... 2009? That's one year.

For his part, Larry Mishel of the Economic Policy Institute argued, "The recession is going to end up accentuating the inequalities of income and wealth we've seen for 30 years," adding, "This requires attention if we're going to see robust wealth growth going forward."

And, as it turns out, begin paying down the national debt.

Between 2001 and 2007- a period during which poverty was rising and average household income had fallen - the 400 richest taxpayers saw their incomes double to an average of $345 million even as their effective tax rate was virtually halved. As Seth Hanlon of the Center for American Progress explained:

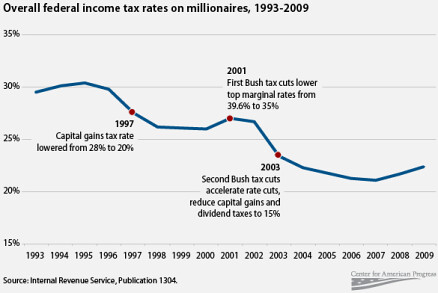

"As a percentage of their incomes, millionaires are now paying about one-quarter less of their income to federal taxes than they did in the mid-1990s...Millionaires paid an average tax rate of 22.4 percent in 2009, down by a quarter since 1995, when they paid an average of 30.4 percent."

But as Americans learned during the Republicans' just concluded debt ceiling hostage taking, the suggestion that the wealthiest people and most profitable corporations pay even a penny in new taxes produces a predictable response from the GOP.

At a time of record high income inequality and historically low federal taxes, Senators Dan Coats (R-IN) and Kelly Ayotte (R-NH) quickly called that common sense idea "class warfare." Utah's Orrin Hatch wasn't content to lament "the usual class warfare the Democrats always wage." (The poor, Hatch insisted, "need to share some of the responsibility.") As for a Senate resolution asking the same of millionaires, Alabama Republican Jeff Sessions said that was "rather pathetic."

What's really pathetic is the all-out Republican defense of the likes of Warren Buffett, who explained, "It's my class, the rich class, that's making war, and we're winning."

And in this tale of two recessions, if you have to ask who won the class war, the answer is simple. Not you.

(This piece also appears at Perrspectives.)